| |

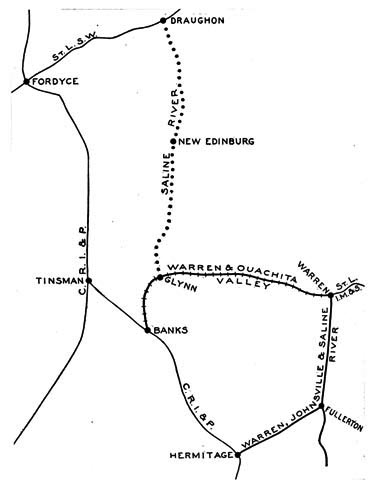

WARREN & OUACHITA VALLEY RAILWAY. The Warren & Ouachita Valley Railway Company was incorporated in 1899 and has capital stock outstanding to the amount of $284,000. It is owned by the stockholders of the Arkansas Lumber Company and the Southern Lumber Company, both of which have mills on its line. There is no bonded or other indebtedness. The officers of the tap line are officers also of one or the other of the lumber companies. The record does not indicate whether there is any intercorporate or other relation between the lumber companies.

The tap line connects with the Iron Mountain at Warren, Arkansas, and extends westward for a distance of about 16 miles to Banks, Arkansas, where it meets the rails of the Rock Island. At Glynn, about 5 miles from Banks, a connection is made with the line of the Saline River Railway Company, as heretofore stated. The lumber companies jointly own an unincorporated logging road extending from a connection with the tap line for a distance of 10 or 12 miles into the timber. Each of the lumber companies also has private logging spurs connecting with the rails of the Rock Island. These unincorporated spur tracks are operated by the lumber companies themselves. In hauling their logs to the mills they have trackage rights over the line of the Rock Island for which they pay 75 cents per train-mile; they pay the tap line 15 cents per 1,000 feet of logs, which is equivalent to about 50 or 60 cents per train-mile, for the privilege of operating log trains over the rails of the tap line to the mills from the junction with the Rock Island or from the junction of the unincorporated spurs with the tap line, as the case may be.

One of the mills is at a distance of 12 miles and the other 2 miles from the connection with the Iron Mountain at Warren; they are therefore nearly 15 miles from the junction with the Rock Island. The tap line hauls the lumber from the mills to the Rock Island, on the one hand, and switches the lumber to the Iron Mountain on the other, the tonnage being about equally divided between the two trunk lines. Out of the joint rates on lumber which are the same from points on the tap line as from stations on the trunk lines in this vicinity, an allowance is made of from 1 to 5 cents per 100 pounds.

The Warren & Ouachita Valley has three locomotives, two passenger coaches, six freight cars, and a caboose. Each of the lumber companies also owns and operates locomotives and logging cars. The tracks of the tap line are laid with 60-pound steel rails and are well ballasted, with permanent bridges. It has a station building at Warren and a telegraph and telephone system. It operates two trains daily each way and its revenue -from passengers is said to exceed $1,000 per month. While more than 5,000 bales of cotton are raised along its line annually, most of this traffic is drayed by the farmers to the trunk lines. The total lumber tonnage for the fiscal year 1910 was 53,830 tons, of which about 7,500 tons was moved for small independent mills on or near its line. More than 90 per cent of its entire traffic and revenue is supplied by the lumber companies in whose interest it is operated. In this percentage is not included the log movement over the tap line performed by the lumber companies themselves. Including this large tonnage the percentage of outside traffic would be comparatively insignificant. In the outside traffic is included the lumber received from the Saline River Railway, amounting to something like 20 carloads per month.

The record indicates that the Warren & Ouachita Valley is a profit-able investment, and this is confirmed by the annual reports made to the Commission. Its total revenue for the fiscal year 1910 was $83,496.09, and its net operating revenue $21,140.35. It paid during that year a dividend of $28,400, partly out of surplus, leaving a surplus at the end of the year of $3,502.93, having paid during the previous three years dividends aggregating 50 per cent on its capital of $284,000.

In this case the controlling lumber companies not only have track-age rights for hauling their own logs over their own tap line to their mills, but have trackage rights for the same purpose over the Rock Island. This we regard as unlawful. We do not understand that shippers may move their property over the rails of common carriers except under lawfully published tariff provisions open to all shippers. As a part of the contract giving its use in that manner to the lumber companies the Rock Island requires them to route half of the products of their mills to its line. The arrangement apparently was a con-cession to the lumber companies for their traffic.

The mills of the controlling companies at Warren are respectively 1 and 1-1/2 miles from the Iron Mountain rails. We think that the Iron Mountain may pay this tap line nothing in excess of a reason-able switching rate, which we fix at $2.50 per car, and that the Rock Island may make a division out of the rate from these mills not exceeding 2 cents per 100 pounds. |

|